| |

The Latest Insight from Ascendant Partners, Inc.

|

|

5347 S. Valentia Way

Suite 250

Greenwood Village, CO 80111

PARTNERS:

Kirk Martin

303.221.4700 Ext. 2

Email Kirk

Scott McDermott

303.221.4700 Ext. 3

Email Scott

Mark Warren

303.221.4700 Ext. 4

Email Mark

Sue Wyka

303.221.4700 Ext. 7

Email Sue

|

|

|

|

|

|

Successfully Building Organic Supply Chains

|

Opportunities to capture value through integration.

|

A common refrain repeated by our customers is that the growth of the organic sector is constrained by a shortage of organic handling and processing infrastructure. Building out this infrastructure is critical to ensuring that the first link in the supply chain, the grower, can profitably produce organic crops and bring them to market. For a grower deciding between continuing to produce conventionally or organically, one of the first steps they take is understanding the closest available market for their crop. If their immediate area lacks an organic market, someone who will readily take organic production, they are likely to continue growing conventional crops. As organic demand continues to grow, supply has been slow to follow. While the problem isn't as easily seen in the fruit and vegetable producing regions of California and the Western US, other areas of the country have been slow to adopt organic practices due to higher production costs, increased risk, and a lack of adequate infrastructure. In this quarter's insight, we'll look at opportunities in the organic production supply chain and some of the reasons industry participants have been slow to adapt to demand for organic goods.

|

|

|

|

|

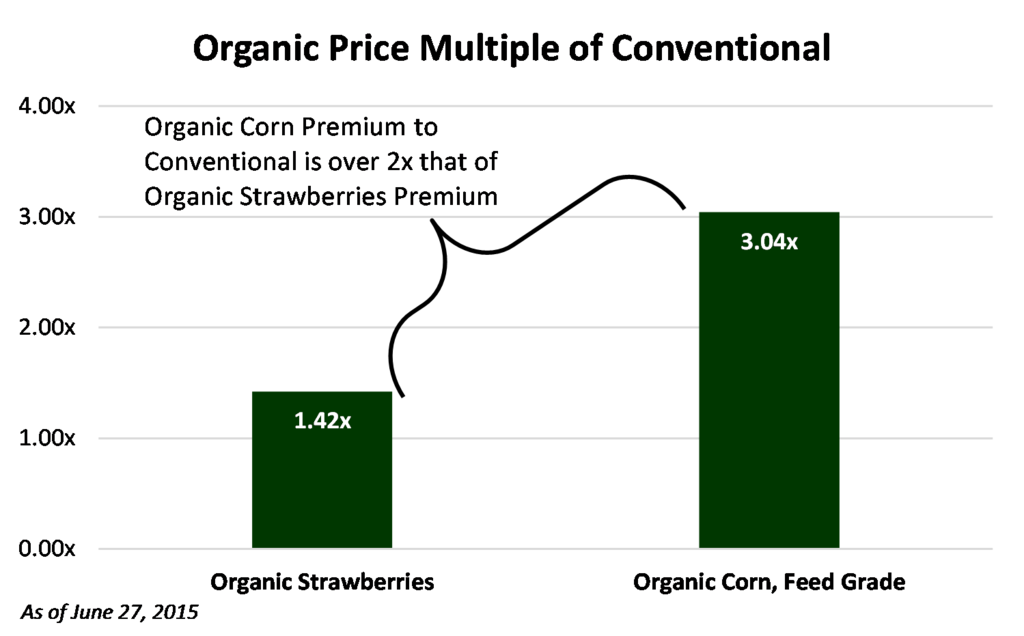

Opportunities for those who overcome the supply chain challenges described below are the substantial premiums for organic production. Particularly, in the grain markets where the supply chains haven't widely adopted organic production, as highlighted below with the organic corn premium over 2x the premium for organic strawberries.

The organic grain and oilseed returns per acre further illustrate the investment potential. While the returns to the organic producer are substantial, despite lower yields, relative to conventional crops, those returns may be eroded from supply chain inefficiencies such as increased transportation costs and loss due to inadequate organic storage capacity. Integrating supply chains is critical to driving the cost of production down and capturing more of the organic premium.

Establishing a supply chain in the organic sector can be difficult and requires careful analysis and a concerted effort on the part of growers and processors. Adding an additional layer of complexity is the way in a which the supply chain is aligned to effectively control and ensure access to supply. Contracting with growers, securing the means of production (vertically integrating), grower profit sharing, or establishing a cooperative/grower-owned structure are all viable ways to ensure access to organic production. While developing the supply chain takes time, that time is rewarded through adding value to day-to-day activities and maximizing the value of organization when the owners exit. Niman Ranch and Applegate are two recent examples of branded food companies with an integrated supply chain with contracted livestock production that met their specific needs. By securing the supply chain a company is able to better secure supply, add value to their organization, and create a barrier to entry in the highly competitive organic and natural food sector.

Based on our experience and conversations with market participants, we've highlighted several common obstacles faced by those in the organic agriculture sector.

Segregating Organic and Conventional Production

Many processors face the challenge of balancing organic and conventional production and avoiding issues like cross-contamination and efficient transitions of different product lines when they only have one facility. Agriculture producers face this same problem but are forced to deal with it in different ways. For example, if a farmer in Illinois wants to plant both conventional and organic they often have 100 or more feet between fields to make sure the fertilizers, pesticides and other chemicals utilized for conventional production don't find their way into the organic field.

3 years. That's how long it takes for a farm operation to become certified organic. During those 3 years, producers often aren't able to realize the full value of organic prices but are incurring the extra costs of organic production. For any producer that is making the decision to continue growing conventional crops or organic, this is a big factor to consider. In addition, producers are faced with the same challenges that processors face in navigating the certification process and various agencies that are involved. Avoiding the common pitfalls and maintaining the proper records are also a challenge for producers and processors alike.

Supporting Infrastructure

We've mentioned this previously, but without the supporting infrastructure needed many producers won't consider organic. For example, if a local market doesn't exist for a grower's organic crop they are forced to transport the crop to the next nearest market which may erode the potential premium received for the organic crop. We've seen several instances where a producer will vertically integrate their operations to remove their reliance on 3rd parties. This is costly, requires additional resources and skills and without sufficient production requires sourcing production from other producers.

Scale is a problem faced in all industries. In industries with greater regulatory or other burdens the challenges are more acute for small companies that lack the scale and resources to overcome those burdens. Organic producers face additional record keeping requirements for the certification process, additional costs of production and an evolving regulatory environment that is often unsupportive of small or medium-scale producers. Sale and distribution of product is another example where it is beneficial to have greater production for spreading costs.

Finding new suppliers is a challenge for producers faced with the decision to produce organics. Many producers are reliant on a sophisticated network of dealers and suppliers to provide them with the necessary equipment and supplies to grow a conventional commodity. In addition, there is a strong sense of community and producers will often share resources between themselves. A producer that makes the change from conventional to organic will not only have to make changes in where they buy their inputs but they also remove themselves from the network of neighbors they rely on.

|

Transaction Profiles.

As we round out the summer and head into the fall, 2015 continues its streak of strong M&A activity despite recent stock market volatility. According to the most recent data from Dealogic, 2015 deal activity is at $3.24T and nearing 2007 records of $3.43T. Whitewave continues to be active and is highlighted again this quarter along with Perdue Farms and Flower Foods.

is Acquired by Whitewave - August 2015 is Acquired by Whitewave - August 2015

Deal Terms: $125MM

2.8x Sales

Wallaby produces a number of products ranging from Greek and Australian yogurt to kefir beverages. The company has been around for 20 years and had $45MM in sales over the previous 12 months. The acquisition by Whitewave strengthens its postion in the $1.2B yogurt category which is highly contested given its high growth rates relative to other categories. In addition, the acquisition provides Whitewave with a West Coast production facility to complement its recently opened Pennsylvania yogurt plant. Many will be watching the category to see if the brand is the right one for Whitewave to compete in this highly contested category.

& &  are Acquired by Flowers Foods - August & September 2015 are Acquired by Flowers Foods - August & September 2015

Deal Terms: Dave's Killer Bread Alpine Valley Breads

$275MM $120MM

1.7x 2016E Sales 1.3x 2016E Sales

In one month, Flowers Foods, the owner of Nature's Own brand bread, acquired Dave's Killer Bread, the leading organic bread company, and Alpine Valley Breads, an organic, non-GMO bread maker headquartered in Arizona. The combined companies will add just over $250MM to Flowers Foods 2016 sales based on current estimates. More importantly, in a nod to the trend we continue to see in the natural and organics category, the acquisitions give Flowers Foods a place in the fast growing organic bread category. The company indicated the category has averaged 25% growth over the last 4 years. Alpine Valley Breads is similar to Dave's Killer Bread although slightly smaller with $90MM in 2015 estimated sales compared to $165MM at Dave's. Both brands are certified organic and non-GMO.

is Acquired by Perdue Farms - September 2015 is Acquired by Perdue Farms - September 2015

Deal Terms: Not Disclosed

The acquisition of Niman Ranch by Perdue Farms marks the next chapter in the natural and organic protein market that last was abuzz with the Applegate acquisition by Hormel. Similar to Applegate, Niman Ranch utilizes a network of 700 farms to produce a variety of beef, lamb, and pork products along with cage free eggs. The company counts Chipotle Mexican Grill among its customers who use its premium products. Perdue, one of the largest poultry companies in the US, will be working to utilize its marketing and distribution networks to expand the reach of Niman Ranch products throughout its supply chain. The acquisition will allow Perdue to expand its reach in the premium meats market and also expand its processing capacity. Niman Ranch was a portfolio company of LNK Partners. While the focus has been on Niman Ranch, the deal also includes SiouxPreme Packing plants in Iowa and Prairie Grove brand of pork products.

|

Earnings Spotlight.

The earnings spotlight highlights several companies in the natural food, commodity processing, and protein industries.

|

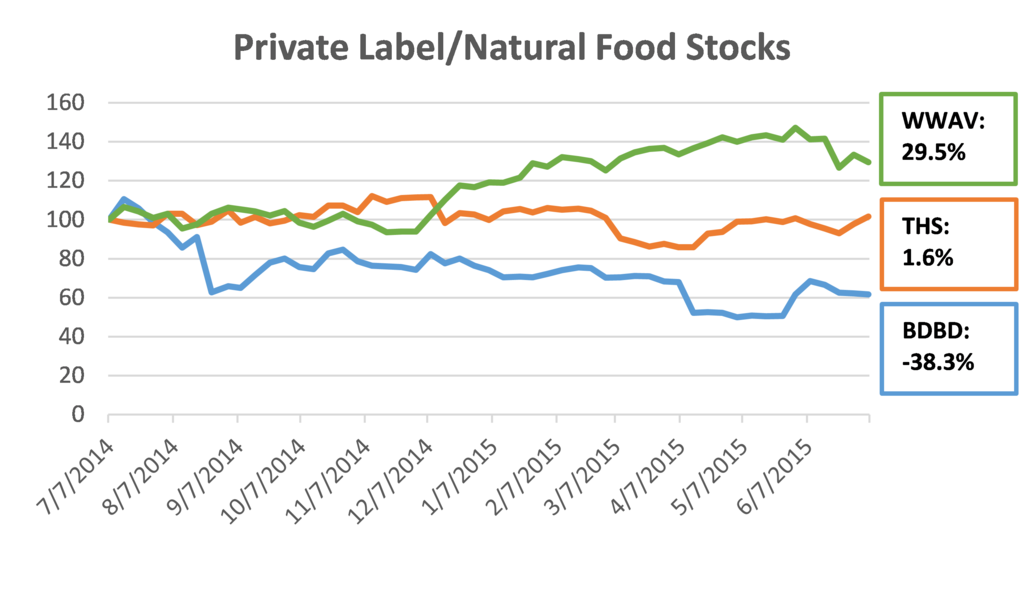

WhiteWave Foods (WWAV) - WhiteWave's stock price reflects its continued streak of strong operating results driven organically and through acquisitions. Including acquisitions, sales grew 10% from 2014 to $924MM for the quarter ended June 30. Management indicated it expects additional organic milk supply over the next 12 months alleviating tight supply conditions. Estimates for 2015 sales growth were increased to 15-16% due to strong 1H15 growth and contributions from acquisitions.

Boulder Brands (BDBD) - Operations continue to fall short of expectations which has lead the Board of Directors to authorize exploration of strategic and financial alternatives to increase shareholder value. The company lost $3.3MM for the quarter compared to a gain of $2.8MM last year.

While distribution has grown, including a deal with Target, sales velocity has remained weak. Competition and potential slow down in the gluten-free category and the competitive spreads category has also dampened results.

Treehouse Foods (THS) - Headwinds continued to face the competitive single-serve coffee category this quarter. The avian flu also negatively impacted results. The company lowered its full year guidance citing the single-serve coffee category as the biggest driver for the lowered guidance. Management indicated that aggressive pricing by Keurig Green Mountain has resulted in a 20% year over year decline in prices. Management commented that their 52-wk coffee pod market share fell to less than 50% from over 67% a year ago and that Keurig Green Mountain captured all of this loss.

|

|

|

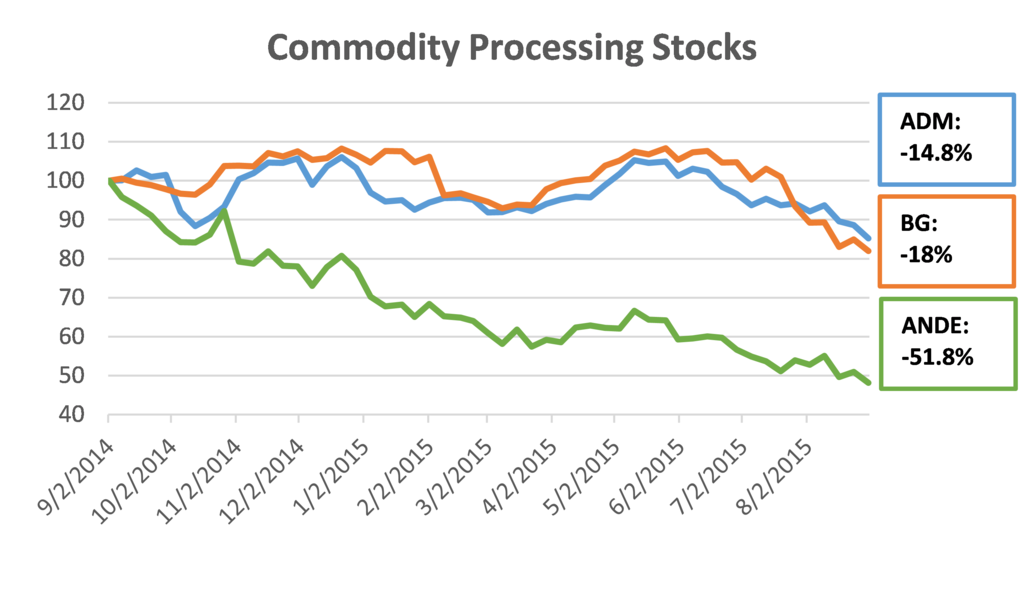

ADM (ADM) - Earnings for the quarter fell 28% from last year to $386MM. A majority of this decline is explained in the lower ethanol earnings which fell $80MM to $188MM due to lower margins from record industry production. Management continues to highlight the Wild Flavors and Specialty Ingredients group and its significant business development pipeline as it seeks to provide products for the current consumer trends.

Bunge (BG) - Results missed expectations as oilseed processing margins in Canada and Europe fell. The company's Brazilian food and ingredients segment was hurt by the negative economic environment in Brazil. Looking forward to the 2H of the year, Bunge expects an improvement as current crop conditions should allow for greater capacity utilization and demand supports favorable crush margins.

The Andersons (ANDE) - Poor growing conditions continued to hurt the plant nutrition group as earnings fell 30% to $31MM from 2Q14. The ethanol group also contributed to the decline in earnings as its earnings declined to $9.7MM from $33.9MM in the previous year's quarter. The company is optimistic for the second half of the year as the grain group's performance improves and the other groups remain steady.

|

|

|

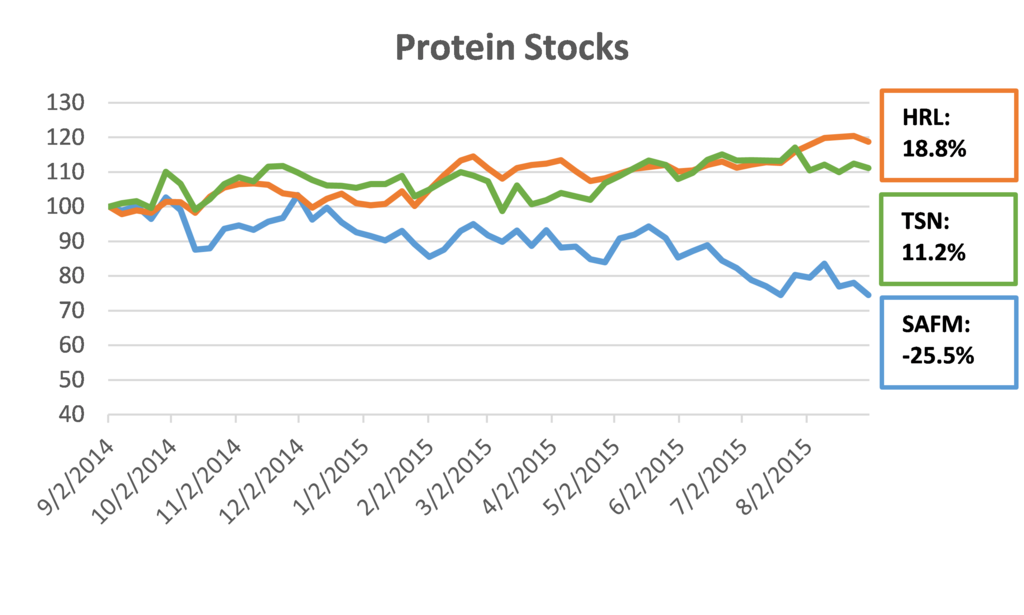

Tyson Foods (TSN) - While the company reported higher quarterly earnings from the previous year it lowered full year guidance due to weak beef markets. The beef segment reported a loss of $7MM compared to operating income of $101MM the year before due to lower volume from feedlots and port issues causing them to market product in lower value markets. The prepared foods segment had strong results as the Hillshire acquisition and synergies related to the acquisition were realized.

Hormel (HRL) - Fears over the impact the avian flu would have on the Jennie-O turkey segment were realized as segment profits declined 45% from the previous year. Despite difficulties from the avian flu and increased pork prices, the company increased its non-GAAP earnings for 2015 to $2.57-2.63 per share, a 15-18% over 2014's record earnings.

Sanderson Farms (SAFM) - Sanderson reported results slightly below last year as import bans due to avian flu affected the price received at their big bird facilities. Compared to 3Q14 boneless breast meat prices were 25% lower for the quarter. Feed prices helped offset this decline with corn and soybean meal prices declining 13% and 35%, respectively from 2014. The company also indicated that its newest plant in Palestine, TX is at 50% capacity and they have broken ground on another plant in St. Pauls, NC.

|

|

|

Thank you for allowing us a moment of your time this quarter. If you would like to discuss this or other topics or if you have suggestions for future issues, please don't hesitate to reach out to us. Our goal, as always, is to add value for you. Any replies will go directly to Ascendant.

- The Ascendant Partners Team

|

|

|

|

|

Copyright © 2015. All Rights Reserved.

|

|

|

|