| |

The Latest Insight from Ascendant Partners, Inc.

|

|

5347 S. Valentia Way

Suite 250

Greenwood Village, CO 80111

PARTNERS:

Kirk Martin

303.221.4700 Ext. 2

Email Kirk

Scott McDermott

303.221.4700 Ext. 3

Email Scott

Mark Warren

303.221.4700 Ext. 4

Email Mark

Sue Wyka

303.221.4700 Ext. 7

Email Sue

|

|

|

|

|

|

Investors are Hungry for Food Companies

|

Why are Investors Interested in Smaller Branded Food Companies?

|

From our vantage point it seems that the food industry deal activity is increasing with a new deal announced almost daily. Through our involvement with Naturally Boulder and our contacts in the food industry, we get a first hand look at the innovation and trends occurring in the natural and organic food industry. Recently, Naturally Boulder hosted their annual Spring Fling.

These events offer an opportunity for members to reconnect and showcase their products. This year's event was well attended by food companies and investors from across the country hoping to get a glimpse at the next rising food companies. While the attendance growth at these events continues to impress us it's an anecdotal example of the continued interest and increased number of transactions occurring across the industry. In this quarter's insight, we wanted to shed some light on the underlying reasons for this interest.

|

|

|

|

|

At this point in the business cycle we've all heard it several times, but it holds true: Corporations are flush with cash, have sluggish organic growth, and cheap financing options. This combination has given them plenty of avenues to deploy their growing war chests, whether through acquisitions, share buybacks or other uses, companies are finding ways to deploy that cash. On top of these tailwinds, the desire to increase participation in natural and organic food and beverage arena has put them in an acquisitive mode.

Corporations are like cruise ships. They have a lot of amenities and comforts but they're slow and easily passed by nimble speed boats that can change course quickly. Sometimes corporations can innovate and get in front of new trends in their industries, but often they are forced to acquire the speed boats who have innovated new products. There is also the desire to not take on risk that sinks the ship. If a cruise ship takes a wrong turn it risks stranding itself in the middle of the ocean or end up sinking. The bottom line is that smaller companies are responding to changes in consumer preferences and growing rapidly while larger more established food companies are acquiring companies to capture that rapid growth.

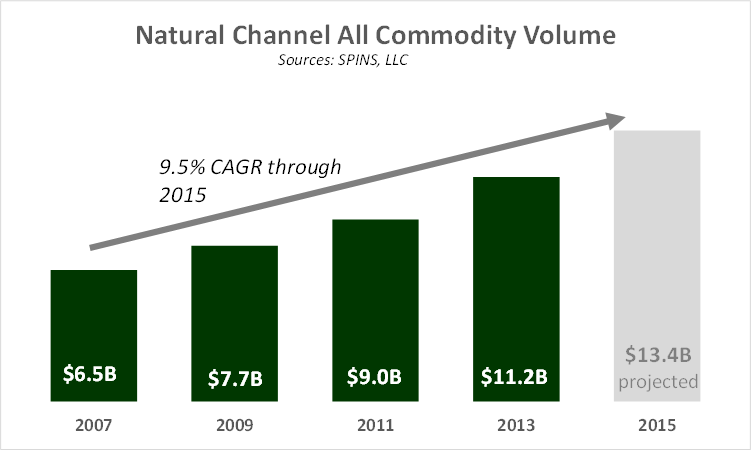

Growth rates from natural and organic products are robust in comparison to conventional products. Based on projected 2015 volume, the industry's growth rate since 2007 has averaged 9.5%. In contrast, many of the heavily processed food categories have had low single digit to negative growth rates. Shelf-stable entree volume, for example, has fallen 20% since 2010. M&A offers an opportunity for companies to capitalize on increased consumer demand for these healthy and nutritionally dense products. Acquisitions of smaller companies also give established brands a conduit to consumers who have lost interest and turned away from legacy brands. Smaller brands offer a story and the intimacy consumers are looking for and retailers are more willing to consider smaller brands for shelf space to attract those customers.

Core Strengths & Operational Efficiencies

Established companies can take a recently acquired brand and instantly realize new sales opportunities and synergies by virtue of their larger footprint. Acquisitions in the food space have been and will continue to be at least partly motivated by operational efficiencies that are realized through combining complementary brands with their existing platforms. Combining complementary product lines with an established platform is particularly relevant in declining food categories. Finally, by taking a smaller company into a larger organization, core strengths of the company can be leveraged in the smaller company. For example, margins can be improved when a company that has a strong distribution capabilities acquires a brand that may have a weak or expensive distribution strategy.

Companies that identify and participate the trends that drive growth have options that are unavailable to companies that are on the outside looking in. Whether it's General Mills or Hormel, companies are interested in buying brands that give them growth. In addition to corporate acquisitions , we've also noted an increasing number of private-equity deals that have been announced, which provide additional capital and other options for growing brands. Some of the capital raises from private equity over the last several months include Live Better Brands, Hail Merry, Sprout Organic Foods, and a local Boulder company, LoveWild Fish Co.

In addition, a company that is in front of these trends has options with retailers and suppliers. Companies with an in-demand brand have options for operations and raising capital that afford them the ability to continue their growth and meeting consumer trends.

|

Transaction Profiles.

As highlighted above, in the last several months have seen a uniquely strong M&A market with a number of acquisitions and investments in the natural and organic space. This quarter we take a look at the Applegate Farms transaction as well as acquisitions made by WhiteWave Foods and Ingredion.

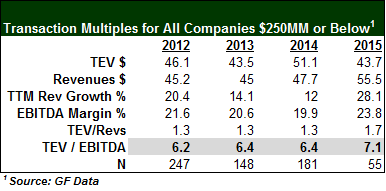

2015 is on pace to exceed the prior to years of M&A activity (see table above). Thomson Reuters reported at the end of June that second quarter deal volume was $1.33 trillion, just shy of the record $1.41 trillion experienced in the second quarter of 2007. This is due to several large transactions that were announced in the second quarter but it's also in part due to the fear some company executives have of missing out on growth while seeing their competitors continue to acquire.

is Acquired by Hormel Foods - May 2015 is Acquired by Hormel Foods - May 2015

Deal Terms: $775MM

2.3x Sales

25-27x EBITDA

The big news in the protein industry over the last quarter has been the acquisition of Applegate Farms by Hormel Foods. Applegate Farms was owned by private equity firm Swander Pace Capital and began the sale process in late 2014. The acquisition is a big step for Hormel which has seen its product mix shift to new avenues outside of its legacy pork business in recent years. The Applegate deal follows several related transactions including Muscle Milk and Wholly Guacamole. As Hormel Foods looks to transition Applegate, it will continue to run it as a stand alone business unit and focus on preserving the valuable Applegate brand which consumers have come to identify as a trusted source of quality organic and antibiotic and hormone-free packaged meats. The deal was announced in May and closed in July.

is Acquired by WhiteWave Foods - June 2015 is Acquired by WhiteWave Foods - June 2015

Deal Terms: $550MM

5.5x Sales

Vega, who offers plant-based nutrition products including powdered shakes and and snack bars, has been acquired by WhiteWave Foods in a deal that values the company at $550MM or 5.5x sales. This represents another deal for WhiteWave in their category expansion strategy and follows their acquisition of Earthbound Farms in late 2013. As the purveyor of nutrient dense products that contain omega-3's and other favorable components, Vega allows WhiteWave to continue building on its current portfolio of plant-based food and beverage items. Vega was found in 2004 and reached sales of $100MM over the last twelve months after growing 30% from 2014. The company was majority-owned by Founder Charles Yang and VMG Partners a private-equity firm focused on branded CPG companies.

is Acquired by Ingredion - July 2015 is Acquired by Ingredion - July 2015

Deal Terms: $100MM

Ingredion, a supplier of starch and sweetener ingredients, has acquired Kerr Concentrates, a fruit and vegetable juice concentrate supplier. This transaction involves two companies that play an important part in supplying ingredients to manufacturers of food and beverage products. Kerr Industries has two process assets in Oregon and California that allow them to produce fresh-packed strawberries, concentrates and purees among a variety of other products. The acquisition helps position Ingredion in the clean label and healthy eating trends and allows Kerr to expand its offerings as part of a larger ingredient company.

|

Earnings Spotlight.

The earnings spotlight highlights several companies in the natural food, commodity processing, and protein industries.

|

WhiteWave Foods (WWAV) - WhiteWave continues its strong performance in 1Q15 with a 17% increase in operating income . In addition management increased their full-year guidance for net sales to low-double digit growth. Growth continues to occur across all segments and brands for WhiteWave and its stock price has responded favorably in spite of tight nut and milk supplies.

Boulder Brands (BDBD) - Boulder Brands has had several big changes over the last several months and its stock price has fallen almost 47% over the last year as a result. The founder and CEO of the Company, Steve Hughes, resigned and was replaced by interim-CEO Steve Leighton in June while at the same time the Company announced it expects 2Q sales to drop 7%. Competition in the gluten-free category and declines in its spreads business continue to plague the company.

Treehouse Foods (THS) - 1Q results followed the path of 4Q results and disappointed investors. Single-serve coffee margins were squeezed by over-supply in the market and less than expected growth in the snack food business were the drivers of the lackluster 1Q results. Despite the results, the Company is optimistic it will see growth in 2016 and continues to look at acquisitions with nearly $400MM available under its revolver.

|

|

|

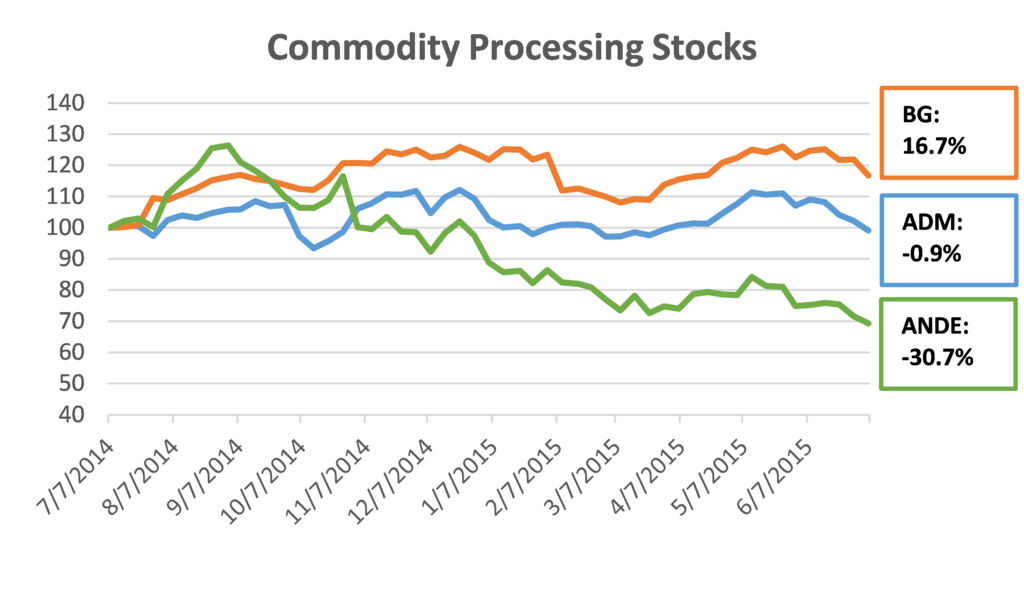

ADM (ADM) - Results were favorably impacted by the Wild Flavors acquisition and strong results of the oilseeds business. The Wild Flavors and Specialty Ingredients segment has been busy integrating several of its transactions and building a robust sales pipeline of 400 projects. The Company remains optimistic for its ethanol business with strong export markets in Q1.

Bunge (BG) - 1Q results were driven by strong oilseed crush margins, similar to ADM results. The oilseed business increased its EBIT year over year from $79MM to $212MM in the 1Q. These strong results were partially offset by weak sugar and bioenergy results of ($23MM) for the quarter. In addition, the Company announced a $500MM common share repurchase program and increased its dividend from $0.34 to $0.38 per share.

The Andersons (ANDE) - In May, the Company completed an acquisition of Kay Flo Industries, a manufacturer of liquid fertilizers and other plant nutrients for growers in the Western Corn Belt. Kay Flo has approximately 100,000 tons of liquid storage which support sales of 200,000 tons per year. For the quarter, the ethanol business produced a record amount of gallons with 93.2MM for the quarter. Poor weather for planting impacted the Company's results and were blamed for a 82% drop in reported gross profit.

|

|

|

Tyson Foods (TSN) - Quarterly results for the company beat management's initial expectations with a 51.5% increase in operating profit from 1Q14. Prepared Foods and Chicken segments helped carry the day for the Company's 2Q results as the Chicken segment posted $1B in operating profits over the last 12 months. In addition, they have realized $77MM in synergies from the Hillshire acquisition, ahead of their original estimate for the year of $225MM and have revised their estimate to $250MM.

Hormel (HRL) - Hormel was involved in the acquisition of Applegate Foods, a leading brand in the natural and organic prepared meat category, which is detailed above in our Transaction summary. Hormel announced record 2Q earnings per share of $0.67 from $0.52. Refrigerated Foods posted a 52% increase in operating profit due to strong sales in food service and retail value-added products. The turkey business, Jennie-O Turkey store, has seen its supply chain impacted by avian influenza that is likely to carry over into next quarter and even 2016.

Sanderson Farms (SAFM) - Tailwinds from lower input costs and strong poultry demand created robust 2Q earnings for the Company. Feed costs were almost 12% lower from the previous year and optimism for this year's crop has kept feed costs low. The Company sees growth in chicken processing of 3-4% in 2015 and another 2.5-3% in 2016. While processing capacity shouldn't be a problem the industry may run into trouble if growth continues to climb after 2016, according to the Company.

|

|

|

Thank you for allowing us a moment of your time this quarter. If you would like to discuss this or other topics or if you have suggestions for future issues, please don't hesitate to reach out to us. Our goal, as always, is to add value for you. Any replies will go directly to Ascendant.

- The Ascendant Partners Team

|

|

|

|

|

Copyright © 2015. All Rights Reserved.

|

|

|

|