Want to start a conversation right now? We are happy to help.

Click Here to get started!

Financial education is not just about the money; it's

about building great families and raising self-confident kids who have the tools to realize their dreams.

Joline Godfrey

|

| AILSA CAPITAL

272 E 12200, Suite 100

Draper, Utah 84020 Toll Free (866) 511-0302

T (801) 501-0302

F (801) 501-0313

San Diego (619) 952-3561 [email protected] Visit us on the web at www.ailsacapital.com |

|

Know someone who needs a trusted source for Wealth management and insight?

Click the link below to send them a copy of this newsletter with a note from you. Let us here at Ailsa know what we can do to follow-up with your referral.

Please let us know if you would like to be invited to any of our upcoming events, we are happy to host you.

|

|

|

The Importance of Long-Term Care Insurance

|

| A new creative way to have long-term care insurance. |

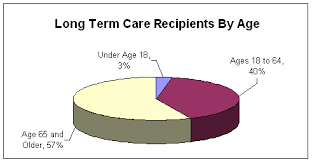

In addition to typical medical expenses in retirement, you should also consider the cost of long-term care arrangements should you need professional care in your later years, either in-home or in an assisted living facility. There's a good chance you'll need assistance, and it won't be cheap. Recent studies have put the odds at 50/50 that a 65 year old will need living assistance in their lifetime. The average period of help runs about 2 years.

According to the 2012 MetLife Market Survey of Nursing Home, Assisted Living, Adult Day Services, and Home Care Costs, the average annual cost for a private room at a nursing home in 2012 was $90,520. The national average for a semi-private room was $81,030. The national average for an individual living in an assisted living community was $42,600.

In most cases, long-term care health insurance coverage provides benefits for nursing homes, assisted living facilities, and home care. If you can afford the premiums, you may want to consider purchasing long-term care insurance.

Many of our clients find that the cost of these policies and the potential for the premiums to increase in the future are prohibitive to them purchasing the insurance. We have found a creative solution that combines long-term care insurance with whole-life life insurance. In this situation, a client would purchase a whole-life policy (for example, $250,000). They then add a long-term care rider onto the policy (cost depending on several factors). The policy works like a normal life insurance policy unless you need long-term care. When you do need help, the policy pays out 1% of the death benefit monthly towards long-term care. In our example, the policy would pay out $2,500 a month as long as the client needed the help up until the death benefit it used up. If the client only uses $50,000 of death benefit on long-term care costs and then subsequently passes away, their beneficiary would receive the remaining $200,000 of death benefit.

We cannot stress enough the importance of planning for retirement costs, long-term care being one of them. We also understand the hesitancy of clients to purchase long-term care costs due to the cost. We have found this whole-life/long-term care duo to be a creative solution to the problem.

Please

contact us to review your personal situation and see if this might be a good solution to your planning issues.

|

|

Teaching Kids About Money $$$

|

There has been a push to teach financial literacy in high school, but it seems

like t

hat push is falling on deaf ears. One thing is certain, kids are not learning valuable money skills at school, so it is up to parents to teach these lessons.

There has been a push to teach financial literacy in high school, but it seems

like t

hat push is falling on deaf ears. One thing is certain, kids are not learning valuable money skills at school, so it is up to parents to teach these lessons.

B

el

ow is a list of some of the important things kids need to know about money.

- Saving. Spend less than you earn. It's such a simple maxim, and yet very few young adults understand it or know how to follow it. Teach your child from a young age to put part of money he receives or earns in the bank. Teach him how to set a savings goal, and save for it, and then purchase whatever it is he was saving for.

- Budgeting. Many of us dread this task as adults, and suffer because of it, because we lack the understanding and skills necessary to make budgeting a breeze. Teach them simple budgeting skills, and what's involved, and they won't have problems as an adult. You could wait until teenage years to do something like this - but it's a good thing because this shows them why basic math is necessary.

- Paying bills. Give them bills to pay and have them pay it on time, online or in the real world. Learn how to write a check, paper and online, and how to make sure that you're never late with bills again - either pay them immediately or automatically.

- Investing. What is investing and why is it necessary? How do you do it and what are different ways of doing it? How do you research an investment? How does it compound over time? This is a good conversation to have with your teen.

- Frugality. This is something to teach them from an early age. How to shop around to get a good deal, to compare between products of different prices and quality, to make things last and not waste, to cook at home instead of eating out too much, to control impulse buying. When we go out and do a shopping spree, including before Christmas, we are teaching them just the opposite.

- Credit. This is a major problem for many adults. Teach them the responsible use for credit, and how to avoid it when it's not necessary, and how to avoid getting into too much debt, and how to use a credit card responsibly.

- Retirement. Is it better to work hard and retire or to take mini-retirements throughout life? That's a personal question, but your child should be aware of the options and the pros and cons of each, and how to do each. Why it's important to start investing in retirement when you're young, and how much of a difference that can make through compound interest. How to do it automatically.

- Charity. Why this is an important use of your money, and how to make it a regular habit. This should be not only a financial issue, but a social one. Show them how to volunteer their time and effort as well.

If you want more help on ideas and ways to teach kids about money, Joline Godfrey has authored a great book called, Raising Financially Fit Kids. See the link above for how to get your own copy. If you want more help on ideas and ways to teach kids about money, Joline Godfrey has authored a great book called, Raising Financially Fit Kids. See the link above for how to get your own copy.

Conversations with your kids about money, the small, grand and grown kind, can be tricky.

Your Ailsa Capital advisor is always happy to talk through your questions.

We enjoy educating others in financial topics, let us know if we can be of help.

|

|

|